Housing Market Offense: Feds Make It Easier For First Timers To Buy In

At the start of the fall parliamentary session, the Liberal government announced changes to mortgage rules to spur purchases of new builds and make it easier for first-time home buyers to get on the property ladder. These changes are set to take place on December 15, 2024.

The biggest change was increasing the cap for insured mortgages to $1.5 million from $1.0 million, making it easier for more Canadians to qualify for an insured mortgage with less than a 20% downpayment.

The previous $1 million cap meant that homebuyers with less than 20% down could only buy homes valued at $1 million or less. To fund a $1 million purchase, these homebuyers had to come up with a downpayment of at least $75,000 (5% down on the first $500,000 and 10% down on the remaining $500,000).

Under the new rules, these homebuyers can now buy homes valued at $1.5 million or less. To fund a $1.5 million purchase, these homebuyers will have to come up with a downpayment of at least $125,000 (5% down on the first $500,000 and 10% down on the remaining $1 million). With the arrival of the First-Home Savings Account (FHSA), which allows prospective home buyers to efficiently save up to $40,000 each, as well as the recent increase to the withdrawal limit under the RRSP Home Buyer’s Plan (HBP) to $60,000 each, up from $35,000 prior to April 2024, funding a downpayment in a one of Canada’s major cities is much easier than before.

This change to the purchase cap is sure to have the greatest impact for buyers in the country’s most expensive markets like Toronto and Vancouver, where the average list prices exceed $1 million. The change is also likely to support house prices in major cities as more buyers are now able to bid on average to above average priced homes. Good news for those anxiously waiting to get on the property ladder but bad news for those waiting for house prices to fall to snag a good deal.

The other major change to mortgage rules is expanding eligibility for 30-year mortgage amortizations for all first-time homebuyers and all buyers of new builds who require a high ratio mortgage (i.e. those with downpayments of less than 20%).

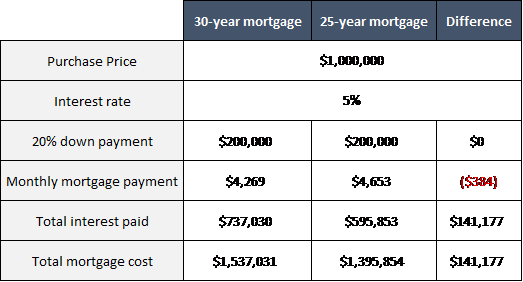

This change will help more borrowers qualify for mortgages by lowering the monthly cost of servicing a new mortgage, helping satisfy lenders’ debt service ratio requirements. Below we see that a homebuyer purchasing a home for $1 million, with a 20% downpayment and a mortgage at a 5% interest rate would see their monthly mortgage payment come in $384 (~8%) lower with a 30-year amortization when compared to a 25-year amortization. The downside is that this borrower will pay an extra $141,177 in interest as a result of maintaining a mortgage for an additional five years.

Like the change to the purchase cap, increasing access to 30-year mortgages will likely see the greatest impact in the Canada’s most expensive housing markets where high monthly mortgage costs prevent some prospective homebuyers from participating in the housing market.

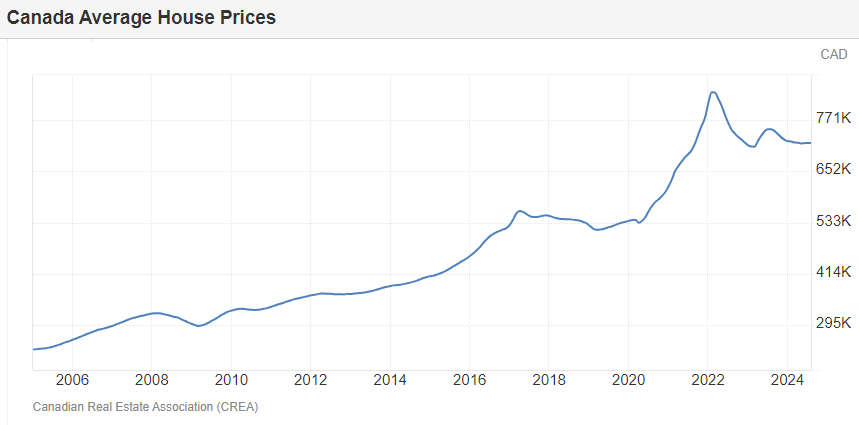

Canadian house prices remain well off their 2022 peak and have been relatively flat for 2 years. Stable housing prices could be seen as resilience considering 5-year fixed high ratio mortgage rates rose from ~1.5% in 2021 to as high as ~6.0% in recent months.

Many housing market commentators have raised concerns that the mortgage rule changes, combined with the expectation of falling interest/mortgage rates over the next 1-2 years, will reignite a buying frenzy in Canadian real estate. Current new home sales activity is beyond weak, hitting an all-time low in the Greater Toronto Area in August 2024. The mortgage rule changes look to stimulate new home construction in particular but developers will respond far more to high and rising housing prices than incremental rule changes that only affect a small percentage of buyers. With a housing shortage expected to be over 3 million units by 2030, and new home sales and housing starts heading in the wrong direction, anything to revive the Canadian housing market seems necessary, even if that means rising home prices and worsening affordability in the short-term.

News and our views

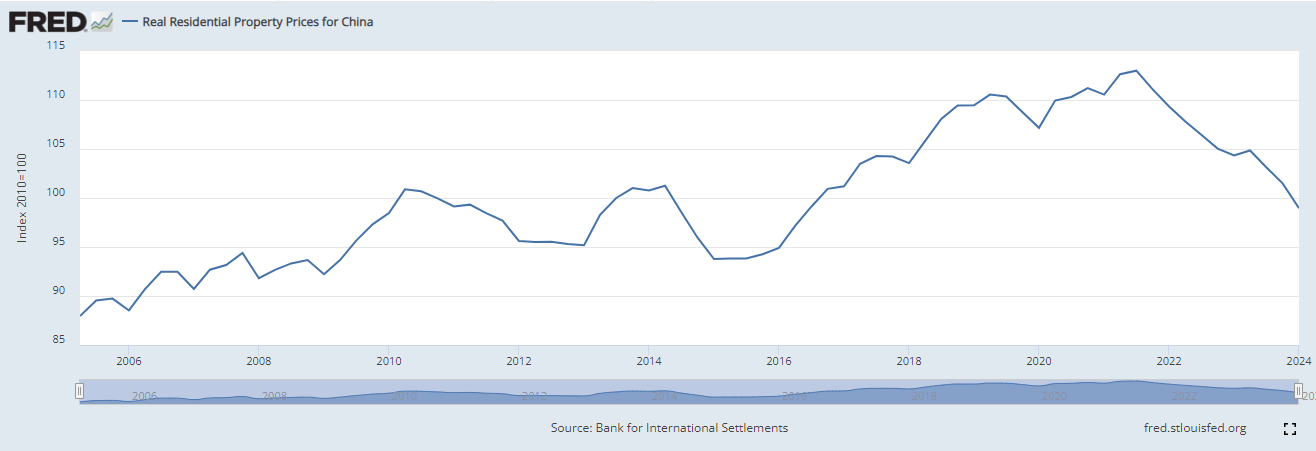

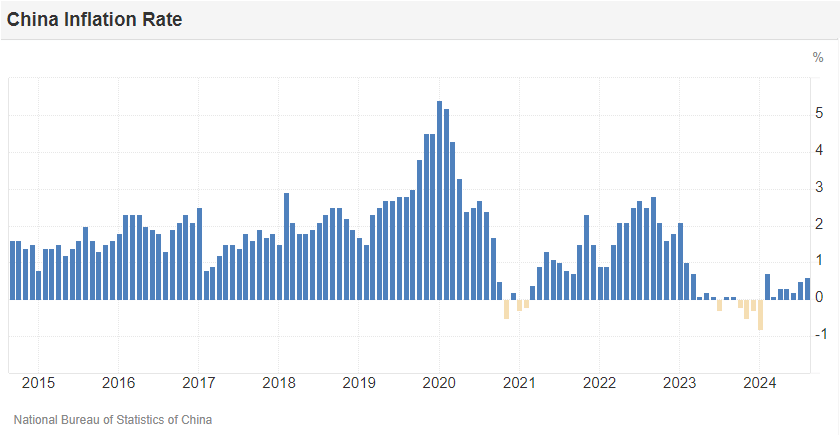

China Unleashes Fiscal Bazooka. For nearly a decade, the Chinese government has attempted to prop up its ailing property market using targeted support aimed at keeping weak developers solvent long enough to allow orderly corporate restructuring or a sale process to healthier developers. This targeted support helped prevent chaos in the Chinese property market but didn’t do much to boost economic growth or help average Chinese citizens. Like the rest of the world, China property prices have been in a slump since 2021. For most countries, a ~15% decline in national house prices over a few years is tolerable but in China, where property accounts for ~70% of household wealth, roughly double that of most other countries, falling property prices can have significant economic and societal consequences. In recent years, falling property prices, weak economic growth, and high youth unemployment, helped accelerate a decline in birth rates triggering overall population declines in 2022 and 2023, decades ahead of expectations. The country’s inflation rate has been near 0% for over a year, another sign that the Chinese economy is unlikely to grow rapidly again without government help. Chinese lawmakers had seen enough in September, cutting interest rates across the board to stimulate household borrowing, cutting bank reserve requirements to boost lending activity, lowering downpayment requirements on second homes, and promising to unleash the country’s most aggressive fiscal stimulus in well over a decade including one-time subsidies to low-income households and over US$100 billion earmarked to support Chinese financial markets.

Our Take: The official stimulus statement included an unprecedented line about the primary goal of the stimulus package – “stabilize the housing market and stop its [price] decline”. This is the first time that Chinese policymakers have set a goal to halt the decline in house prices and to achieve this goal, it may require whatever it takes, which would be positive for Chinese asset prices in general. Admittedly, this feels different this time. In response to the stimulus bazooka news, Chinese stocks posted their best week in 16 years and Hong Kong stocks their best since 1998. Stocks whose profitability is subject to the wills and wants of the Chinese government, such as Alibaba (BABA) and JD.com (JD), saw even greater upside, jumping ~30% and ~50% respectively in the week following the government’s announcement. Seeing that China is the growth engine of the world, a more predictably growing Chinese economy should help boost growth elsewhere around the world as well. Chinese fiscal stimulus combined with falling interest rates around the world could help boost global economic activity in the coming years, which would be well received by equity and bond markets, but it could also raise the risk of higher than expected inflation, which may not be well accepted by equity and bond markets. Either way, emerging market equities have historically outperformed during US Federal Reserve interest rate cutting cycles, and Chinese stimulus may supercharge this outperformance in the coming months.

China Real Residential Property Prices (2010 = Base 100)

Just for fun

- Fair use much?! The UK denies a seven year-old boy a passport due to copyright infringement. In preparation for a family trip to the Dominican Republic, Loki Skywalker Mowbray was denied a passport by the UK Home Office claiming it couldn’t print “Skywalker” because of Disney’s copyright on the name. After cancelling their trip and contacting the media, UK Home Office notified the family that a passport would be issued. Thankfully, the trip is back on now that all is sorted out.

- Kroshik (Crumbs) the Giant, an almost 38 pound cat, fumbled his escape attempt from a Russian fat camp, getting himself trapped in an unassuming shoe rack. Kroshik reached this incredible weight hoovering up cookies and soup. That’s a lot of borscht! For reference, the lasagna monopolizing cat by the name of Garfield fictionally clocks in at 27 pounds. Kroshik is fatter than fiction and will probably not live well without change. Back to fat camp you go Kroshik!

![]()