Canadas Aging Population Could Turn The Current Labour Shortage Into A Permanent One

Canada’s Aging Population could turn the current labour shortage into a permanent one

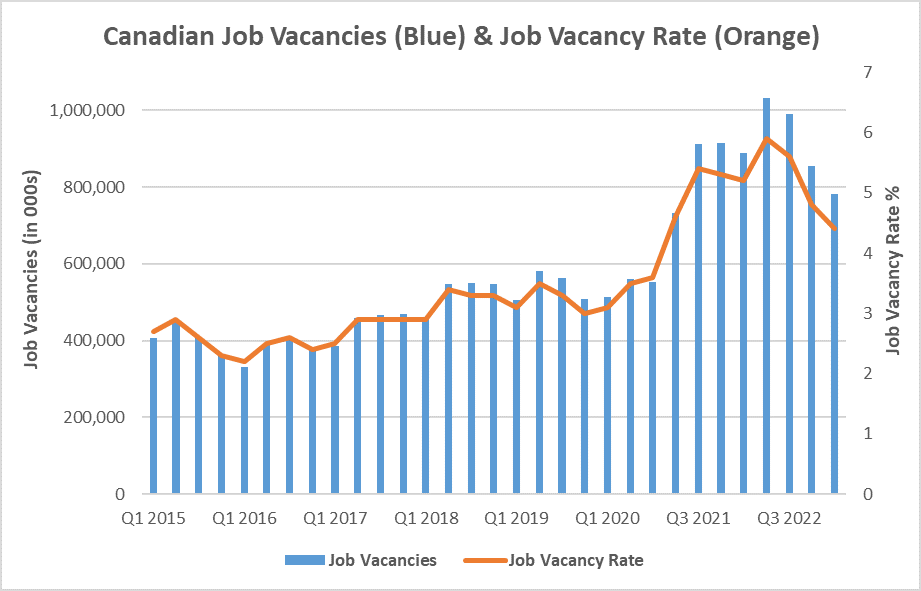

The number of job vacancies in Canada spiked following the start of the COVID-19 pandemic as government stimulus kept households and businesses spending on goods and services and government subsidies, designed to prevent undue business hardship due to COVID, paused the business cycle and with it sidestepped a rise in cyclical unemployment that routine business bankruptcies bring about.

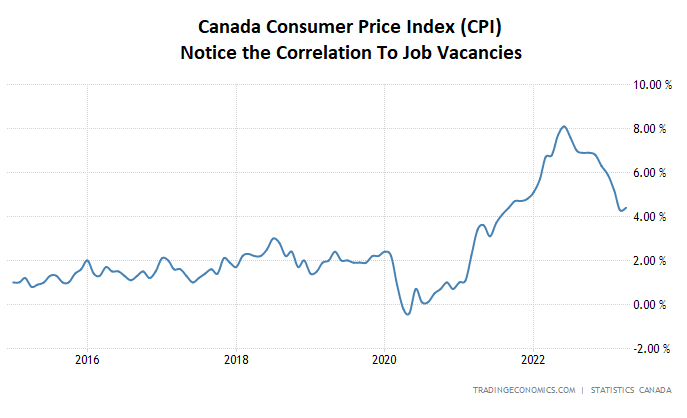

A large part of the inflation problem we face today in Canada is a direct result of these policies. This is also why high inflation is a problem in most economies around the world as the governments of nearly all countries pursued similar stimulus and subsidy programs during the pandemic.

Since early 2022, central banks around the world have been trying to offset the effects of these subsidies and stimulus – high inflation – by raising interest rates. Higher interest rates slow economic activity by reducing discretionary income and savings, boosting the business bankruptcy rate and in turn boosting the unemployment rate, which in the past has reliably brought down inflation over time. This is the go-to play in the central bank playbook and is a tried and true way of boosting cyclical unemployment in a bid to tame excessively high inflation.

We know a good portion of Canadian job vacancies are low skill jobs that do not pay well, have unattractive hours and/or have little room for advancement. Many of these job vacancies will likely go unfilled and will be pulled by employers due to either spending cutbacks or business bankruptcies as businesses face the full brunt of higher interest rates and weak consumer demand. This is the maneuver that central banks are attempting to pull off and is one they have pulled off numerous times in the past. That said, we also know that there are signs of longer lasting structural dislocations in the labour market as result of the pressures caused by the pandemic. The year ending August 2022 saw 32% more workers retire than in the prior year. Nearly two-thirds of these ‘excess retirements’ were in health care, construction, retail trade and education and social assistance, fields that are expected to see greater than average demand for workers in future. While these excess retirements were likely caused by burnout or other pandemic specific reasons, the effect of the excess retirements only exacerbates the structural problems posed by an aging population.

The 2021 Canadian census showed that 21.8% of Canadians are close to retirement age (between 55 and 64 years old), an all-time high for Canada. There are now 81 persons aged 15 to 24, the ages individuals typically enter the labour market, to every 100 persons aged 55 to 64, showing that we will start to see our labour market, ex-immigration, shrink. In 1966, this ratio was 200 persons aged 15 to 24 to every 100 persons aged 55 to 64, so quite the shift.

Structural unemployment is seen as a mismatch between the skills that workers in the economy can offer and the skills demanded of workers by employers. According to StatsCan, “employer’s difficulties to fill job vacancies requiring high levels of education cannot, in general, be attributed to a national shortage of highly educated job seekers or to local shortages of such job seekers”. This is because there is an ample number of highly educated job seekers to cover the vacancies of highly educated jobs but highly educated jobs are not homogenous and highly educated job seekers cannot fill all types of highly educated jobs. These job vacancies are often more essential than not – think nurses, doctors, teachers, plumbers, electricians, etc. – and employers’ demand to fill these jobs will rarely go away in response to higher interest rates. Elevated numbers of high skilled job vacancies will undoubtedly push wages higher for these occupations as employers fight over an insufficient number of skilled workers, something we saw during the pandemic and a core reason for high levels of inflation we’ve experienced in recent years. If the labour market problem we face ends up being a structural one, at least partially, we may see somewhat higher than expected inflation in the coming years or decades.

Thankfully, there are levers we can pull as a society to ease the pressure of structural employment shortages. One important lever is downshifting, something we discussed earlier this year. Keeping skilled workers in the labour force for longer will help ease labour market shortages and help reduce the inflation pressures associated with labour shortages, benefitting us all. We have seen the effect of labour shortages in the course of our business in the accounting and tax consulting fields. It is now incredibly difficult to engage an accounting firm to file personal or sometimes even corporate taxes due to a shortage of qualified accountants. This has resulted in higher tax preparation fees (i.e. inflation) and some taxpayers being unable to attain the services of an accountant firm, which could result in negative consequences, come tax time.

A recent StatsCan survey showed that more than half (55%) of people planning to retire would continue to work part-time if they could work part-time and nearly half (43%) would continue working if their work was made less stressful or physically demanding, so the demand for downshifting is there. If you are a businessperson with any sway in HR decision-making, find a way to let your employees downshift as they approach retirement age, and downshift yourself if possible, to help put a lid on inflation for us all.

News and our views

Rising Energy Prices Likely to Pressure Inflation Higher in the Coming Months. Energy prices have rallied in the past two months, with oil (WTI), natural gas (Henry Hub) and gasoline (NYMEX) rising ~21%, 15% and ~22% respectively from their June lows (as of August 16). In Europe, where natural gas supplies could be tight once again this upcoming winter, the natural gas benchmark price (TTF) rose more than 60% from the June lows. The Canadian consumer price index (CPI) rose 3.3% year-over-year in July, ahead of expectations of 3.0%, after falling steadily since June 2022. Inflation is similarly expected to pick up in the US in the coming months largely due to higher energy prices.

Our Take: These data points are early signs that the fight against inflation may not yet be over and interest rates may remain high for the foreseeable future. That said, the effect of higher interest rates has yet to be fully felt in the broad economy, as interest rate hikes generally aren’t fully felt until 9-12 months after each hike, so a further deceleration in economic growth is likely, which should help tame inflation pressures in time.

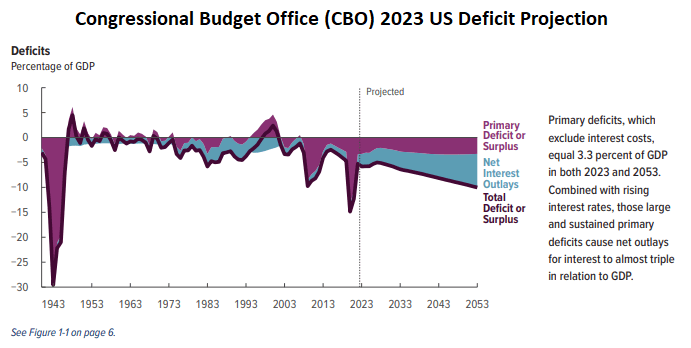

Fitch Downgrades US Long-Term Bond Ratings to AA+ from AAA. On August 1, Fitch Ratings cut its US credit rating from AAA to AA+. Fitch cited that the rating downgrade reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to peers that have a AAA rating. Fitch also highlighted that the short-to-medium term economic outlook is weak and this will pressure tax revenues while there is long-term budget uncertainty regarding the funding of Social Security and Medicare, whose trust funds will be depleted by 2033 and 2035 under current laws.

Our Take: Another rating agency, S&P Global, already downgraded US long-term bond ratings to AA+ from AAA following the 2011 debt-ceiling crisis. Many of the problems noted by Fitch are shared by other AAA rated countries. Most developed nations have aging populations and this will cause social spending, as a percentage of GDP, to rise over time. Many countries also have historically high budget deficits heading into a weak economic environment so may see budget deficits grow further. The Social Security and Medicare funding issue is unique to the US and poses a long-term budget problem, which will require higher taxation or reduced benefits in order to avoid larger budget deficits in future. It is hard to see how America’s divisive government will easily settle these funding issues, which adds to the uncertainty relative to other developed nations. All that said, the US dollar is and will continue to be the world’s reserve currency and this provides the US government with greater sources of funding than other governments. While the outlook for the US economy and its debt is murkier than normal, it is hard to see how the outlook for the US is much less clear than other AAA-rated nations around the world.

Just for fun

- “Gambler: Secrets from a Life at Risk” by Billy Walters is an autobiography of one of the most successful American sports bettors of all time. In it, Billy details his close relationship with golfer Phil Mickelson and alleges that Mickelson has wagered more than $1 billion on sports bets and lost a total of ~US$100 million over his lifetime. This compares to his lifetime PGA Tour earnings of ~US$97 million but is a fraction of his lifetime endorsement earnings of ~US$750 million. You can be sure ‘ol Lefty still has a few hundred million saved up for a rainy day, or possibly more sports bets.

- Pumpkin Spice Season is here! Queue the airwave-monopolizing ad campaigns courtesy of Starbucks and Tim Hortons! Interestingly, Krispy Kreme threw its hat in the ring this year, launching autumnal flavoured drinks and donuts. If leaving the house was a major deterrent to buying one of the world’s most unhealthy but revered delicacies, you’re in luck! For those who are far from a Krispy Kreme store, you can now get Krispy Kreme delivered directly to your door thanks to a partnership with Skip the Dishes. Party on Garth!

![]()